The oil is there. The gas is nearby. The process is proven.

But is there an appetite to put it all together and redefine what it means to be a shale producer? This is the key question looming over the future of enhanced oil recovery for tight shale reservoirs, or simply shale EOR.

To answer it, unconventional oil producers are trying to weigh the options from what amounts to a complicated pros-and-cons list.

Developing a shale EOR program may mean drawing resources away from new exploration projects that have quicker returns, the same conundrum that has stymied the US refracturing market. On the other hand, shale EOR boasts impressive economics for companies willing to reinvest in land and wells already paid for.

This financial tug-of-war has been playing out in the shale sector since the spring of 2016. That was when Houston-based EOG Resources let it be known that its shale EOR program was boosting production from vintage horizontal wells in its Eagle Ford Shale asset in south Texas.

News of the development quickly made the operator synonymous with shale EOR. It is now widely understood that all of these projects rely on the huff-and-puff injection process using natural gas as the special agent that can unlock those additional barrels. Other key details are coming to light as well—such as the expanding scope of success.

In a recent quarterly earnings statement, EOG said it continues to see “strong results” from around 150 EOR wells, more than a third of which were converted in 2018. Analysts and engineering consultants have found about 100 other wells in the Eagle Ford that several other operators have converted into huff-and-puff injectors.

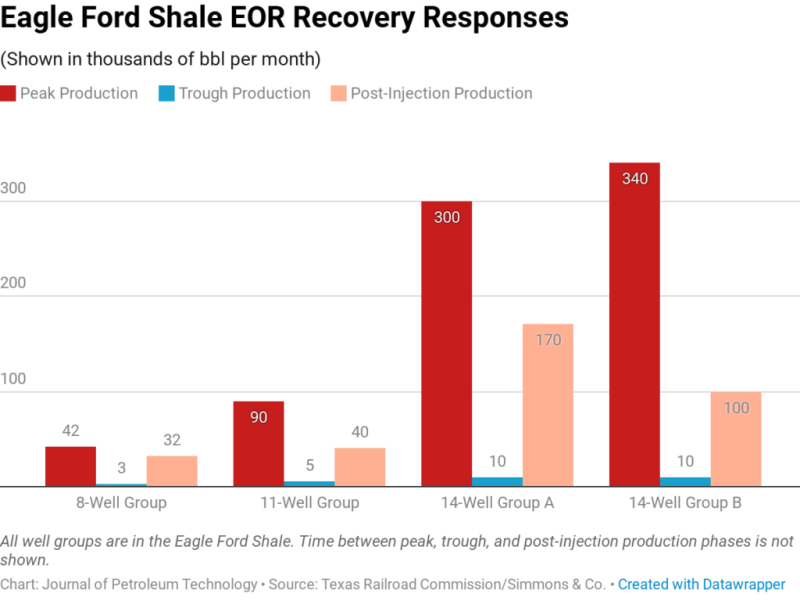

“It’s kind of incredible to see the data,” said John Watson, the senior research analyst who put together a report late last year that highlighted production details of shale EOR projects. After physically combing through filings at the Texas Railroad Commission (since they are not available to download), he found dozens of pad wells that saw a combined 10-fold rise in production above their trough.

Among the standouts, a group of 11 wells that reached a combined peak production rate in December 2011 of about 90,000 bbl a month. By August 2017, these wells were pumping out only 5,000 bbl. After gas injections began, the group produced 40,000 bbl a month—an average increase from about 15 B/D to 117 B/D per well.

Another case involved 14 wells that peaked at 330,000 bbl a month in 2013, then dropped to 10,000 bbl. Post injection, output increased to 170,000 bbl a month.

Watson’s report covers more than two dozen other shale EOR projects, though most lacked production results, revealing only project cost estimates. As opaque as the shale EOR effort has been thus far—at least outside of academic research—operators have shared these eye-openers for one simple reason: they have to. That is, if they want to receive the tax credits eligible for all EOR projects.

“I think there’s still a lot of mystery around what exactly is going on, and I think some of the operators want it to be that way,” said Watson, who as an analyst of the gas compressor market was drawn to investigate the new demand driver for the multimillion-dollar machines that are essential to the process.

Observers and proponents in the engineering consulting sector are emphasizing that the results above are not a fluke. The hard part here is that replicating them requires several factors to come together:

- Fracture networks and fluid properties must be optimal for injections

- Management must be willing to pioneer in uncertain territory and new technology

- The operator has both the time and money to develop the project

- Investors and lenders do not veto the upfront capital investment

Technical Success Is Not Enough

No matter how inspiring or representative the early results appear to be, they have not proven to be enough to warrant major investments by most of the shale sector. Experts believe there are thousands of potential shale EOR locations in the Eagle Ford alone, yet only a relative handful have undergone the process.

Further, less than a dozen shale producers are known to be testing injection operations of various scales in south Texas. A smaller number are understood be moving forward commercially, while another small group are trying to export the technique to horizontal wells in the Permian Basin of west Texas and in North Dakota’s Bakken Shale. Some will rely on CO2, such as Occidental Petroleum’s Permian plans call for, but it appears the most popular approach will rely on natural gas.

Nick Volkmer, vice president of energy research for RS Energy in Calgary, gave one explanation for the cautious approach most operators are taking: “From a technical standpoint, [shale EOR] doesn’t seem as complex to us as discovering how to frac a well. (But) one of the big pieces with this process is that you want to have enough long-term data to be comfortable in that you’re actually increasing overall recovery as opposed to just accelerating production.”

Such certainty will be critical in lowering the perceived risk profile of shale EOR operations in light of the sector’s financial constraints. With access to new capital tightening, the struggle to realize the long-term value of shale EOR appears set to drag on. “It’s a drilling and completions play,” said George Grinestaff, who added that, “These gas injection projects are daunting to [the operators].”

Grinestaff is the founder and chief executive officer of Shale IOR in Houston, one of a handful of engineering consultancies that specialize in the EOR process. The company has used drones and fixed-wing aircraft to fly over the injection sites to confirm the types of equipment being used.

These findings, and other key details, of every known shale EOR project are in a 150-page report that the company is shopping to interested operators. “None of them have failed,” Grinestaff said, of the projects. “They’re all responding in a similar way.”

But barring a significant rise in crude prices, his conclusion is that the sector’s priority will continue to be firmly set on drilling new wells that deliver full returns in their first year. And even though the full benefit of shale EOR can be realized after the first injection cycle—unique compared with conventional EOR—the payout may take up to 2 years because of the cost to “fill up” the depleted wells with gas.

To adopt the long-term vision of shale EOR, producers will be required to redistribute time and resources to the effort. This has given rise to the cottage industry of shale EOR consultancies that believe they can accelerate the project cycle by taking on many of the homework assignments. Though they are bullish on the process, they know shale EOR cannot be done at scale through a cookie-cutter approach.

“You can call me biased, but I don’t think it’s experimental anymore—at least in the Eagle Ford,” said Kaveh Ahmadi, the founder of Pometis Technology, a Houston-based startup focused on modeling shale EOR scenarios to help operators screen candidates. Ahamdi cautioned though that the process “is not a magic bullet” and that, by all accounts, the location of the project is essential to making it work.

One other key aspect he has studied is how long to inject and then soak the reservoir with gas. Ahmadi’s findings suggest that achieving high-enough pressures to maximize, or spread out, the contact area is essential to the process. This also creates a reason to believe that any new barrels of oil that make it to the surface are likely sourced from only a few inches into the rock, at most. “We say the production comes from the near-fracture areas, and that’s it,” said Ahmadi. “If you’re talking about the reservoir as if it contributes, it never does that.”

Another expert, Jeff Rutledge, left Marathon Oil last year after setting up that company’s first shale EOR pilot to start his own firm, QPlus Energy. He too is in the business of designing pilots for other operators and is impressed to see that the earliest EOR projects in the Eagle Ford appear to not have reached their economic limit.

“To me, you just draw the curves and it doesn’t look like it is slowing down, and some of those curves are 3 years old,” he said, referencing the fact that the number of huff-and-puff cycles that each well can go through is limited by the law of diminishing returns. For the shale sector, this is encouraging news since it expands the definition of commercial success.

But achieving success means understanding the reservoir and if its conditions are agreeable to the process. Some of the top factors include API gravity, gas-to-oil ratios, fault locations, external stresses, natural fractures, negative communication due to frac hits, etc. Where all these points align tend to be in the lighter hydrocarbon windows.

Rutledge said this sliver of potentially optimal conditions appears to follow the same geographic trends of the Eagle Ford—which means tens of thousands of horizontal wells could be EOR candidates. “The beauty of it is that, unlike going into a new area, say like in the Permian where you have to pay a lot of money for leases, these are all in existing leases,” he said. “You’re just going back into old wellbores.”

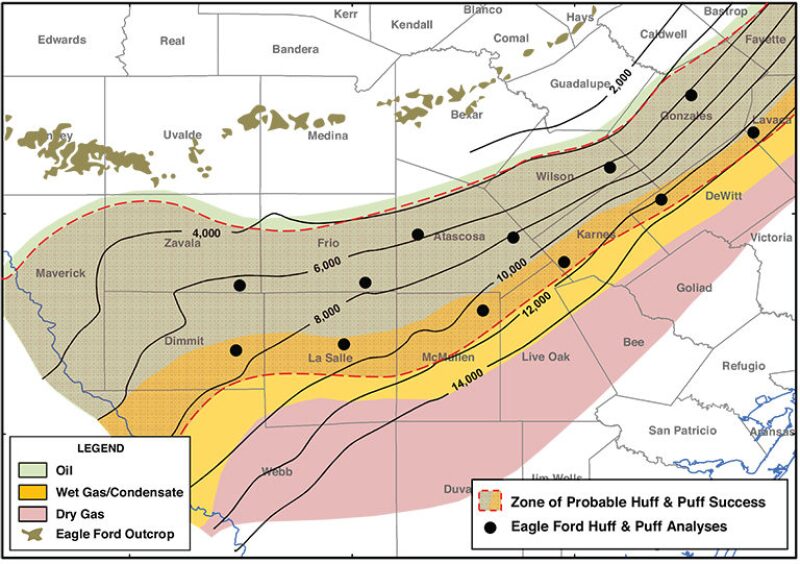

Circled in red are the areas that analysts are researching and believe that cyclic gas injections, or huff-and-puff, will perform best and extract the most crude. Source: GeoMark Research.

What Are the Bottlenecks?

The biggest holdup for shale EOR so far has involved access to the high-horsepower compressors that seem to work best. Chet Ozgen, a technical director with Nitech, a consultancy that has worked on various shale EOR projects over the past 3 years, said the interest in shale EOR has far outpaced the supply of these compressors.

“About 2 years ago, if you wanted to order a gas compressor to inject, you simply could not find one,” he said, adding that the waiting time both then and now is about 12–15 months. Ozgen pointed out that typical field compressors, the kind used to move gas through a sales line, have an upper limit of about 4,000 psi. “Here, we are talking about going up to 7,000 or 9,000 psi, and you don’t just pick those compressors up off the street,” he said.

A leading cause for the scarcity is the $4–4.5 million price tag of the most sought-after compressors, which are often referred to by the model number of their Caterpillar-made engines—the 3606. These high-horsepower engines must be paired with a piece of equipment called a frame that does the actual gas compression, and there are only two firms in the US that supply the full assembly.

The long wait is seen as worth it though, since the 3606 compressors are essential to minimizing the time it takes to see the effects of EOR. Ahmadi said early field results he has access to strongly indicate that “if you want to be successful, go big,” both in terms of the horsepower and the number of wells being converted to huff-and-puff injectors.

The pilots that involve two to four wells on a pad may be good for learning the ropes, however, Ahmadi sees the best returns on what he calls “marquee projects” that involve at least 10 wells. Such large projects might even require two of the large compressor units on the same site. There are multiple factors that dictate performance, but the Simmons & Co. report that shows estimated project economics supports the idea that operators using the most capital are expecting big returns.

For instance, a 14-well injection project in Gonzales County that cost about $16 million is predicted to extract an additional 3.2 million bbl of oil from the lease. In the same county, a three-well EOR project with a bill of $7 million is estimated to add 600,000 bbl of incremental supply.

Grinestaff agrees and said low-cost pilots may fail to achieve economies of scale, and therefore could sour a company’s thoughts on spending much more. “They don’t want to start with $50 million projects,” he said. Getting past the pilot phase though would require such a large sum, so the argument is why not commit to it as early as possible?

Outside of sourcing the compressors, the next hurdle to clear is feeding them enough gas to meet their voracious appetites of about 15 million ft3/D each.

Many locations might have enough supply for a single compressor, but the constraints start to kick in when trying to meet the input needs of more than two. This is an area where EOG is seen as having another major advantage: the company retained its midstream infrastructure while its neighboring peers sold theirs off in recent years to lower operating costs.

A typical compression system for huff-and-puff injections into shale wells. Source: Pegasus Optimization.

What They Are Trying to Figure Out

Once the compressor is on its way to the field, the complexities of shale EOR are only partially solved. “There are such interesting criteria for where this gas injection will work,” said Ozgen, who has high on his list the issue of confinement that is needed to keep the gas near enough to the well’s stimulated zone to drive oil flow.

Confinement. Vertically, confinement in the Eagle Ford, and elsewhere, has so far not been a big concern to practitioners. “Horizontally, we have a bigger problem,” said Ozgen, who explained that the worry here is over the long, tensile fractures that operators created via their early-generation stimulations.

While a large surface area for the gas to interact with is critical to achieving success, there are cases where the tensile fracture networks could be overly extensive, allowing the gas to spread quickly into adjacent wellbores. Ozgen has found that newer generations of hydraulic fracturing designs, ones aimed at generating near-wellbore complexity, are making for the best EOR candidates.

Other Reservoir Characteristics. Operators are turning to the consultants for pressure, volume, and temperature (PVT) analysis to understand how the injections will perform downhole. Rutledge uses PVT reports to find bubble-point data that then allows him to calculate the first-contact miscibility (FCM) pressure of the formation. Knowing the FCM means knowing the pressures at which the rich gas will begin affecting oil flow. Operators are being advised that the bottomhole injection pressure (which is related to the FCM) should not exceed the rock’s fracture gradient, otherwise, new geomechanical complications arise from refracturing the formation.

Soak Times. How long to leave the injected gas inside the formation, known as the soak time, represents yet another big question that companies are trying to nail down during their huff-and-puff pilots. Ahmadi noted that the answer might be simpler than most would expect. “We’re getting to the point where soak time doesn’t matter as much,” he said, justifying the position based on the different cycle times he has seen operators test: 30 days, 20 days, and 15 days.

The results tell Ahmadi that 30 days is too long because diffusion is not the dominant force at play in these wells, and is too slow to economically count on. “Inject as much as you can in the shortest amount of time,” he advised, adding that his studies show that shale EOR is driven by the area of gas contacting the rocks and the pressure—not diffusion.

The shortest cycle time Ahmadi has seen is 20 days and, theoretically, he said a successful outcome could be reached in even less time. “Optimizing the gas injection process means that soak times can be minimized, therefore increasing compressor utilization,” he explained.

Sequencing and communication. The order in which gas injections take place between a group of wells is the key to optimizing the approach. And a big deciding factor here is how the pad wells communicate, which the shale sector has learned is almost always the case.

Ozgen and others are using reservoir models to derisk the sequencing options. Based on his experience, Ozgen estimates that 50% of the scenarios where wells are highly communicative, which could be indicated by a history of intense frac hits during the completions phase, may turn out to be noneconomic. He compared this to converting isolated, individual wells to EOR, in which case the sequencing will have almost no impact on the economics.

In the worst cases, the big risk might be that the wells end up recycling the injected gas from one to the next without improving production. To sum up how critical sequencing is, Ozgen concluded: “If you do not find the correct order, you can lose money and your [incremental] recovery is horrible.”