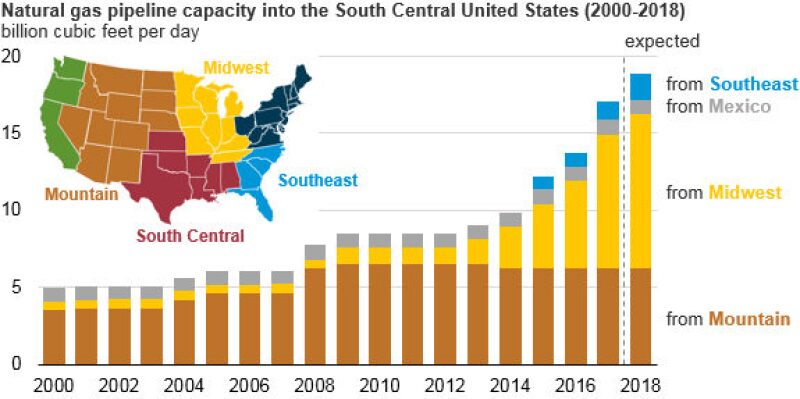

The US Energy Information Administration (EIA) announced last week that it expects natural gas pipeline capacity into the South Central region of the US (Kansas, Oklahoma, Texas, Arkansas, Louisiana, Mississippi, and Alabama) to reach almost 19 Bcf/D by the end of 2018. Natural gas pipeline projects scheduled to come on line later this year will bring additional supply to the US Gulf Coast and support growing export markets, as the region shifts from being a source of natural gas supply to a source of growing demand.

EIA said that, of the additional 6.4 Bcf/D of capacity planned to come on line in the northeast US this year, more than 2.8 Bcf/D will reach the South Central region directly through three projects: Rayne Xpress, Gulf Xpress, and Atlantic Sunrise. Natural Gas Pipeline of America’s Gulf Coast Southbound Phase 1, which will transport up to 0.46 Bcf/D of natural gas from Illinois into south Texas and Louisiana, is also expected to come on line in October. Gulf Coast Southbound Phase 1 is expected to supply the Corpus Christi LNG export facility and pipelines into Mexico.

Natural gas pipeline exports to Mexico are also expected to go up in 2018 as several projects in Texas are completed. EIA said that these exports have grown from 0.9 Bcf/D in 2010 to more than 4.3 Bcf/D in April of this year, and over the same timeframe, pipeline capacity from Texas to Mexico has more than tripled. The completion of the 2.6 Bcf/D Valley Crossing Pipeline will likely continue that upward trend.

Additionally, the Sur de Texas pipeline, currently under construction on the Mexican side of the Texas border, will increase north-to-south flow on the Texas Eastern Transmission Corporation’s (TETCO) pipeline system by 0.4 Bcf/D. Natural gas exports to Mexico will vary based on whenever the facilities on both the US and Mexican side of the border come on line.

EIA said that the LNG export facilities in the US that are scheduled to start up this year and next will represent an additional 6.1 Bcf/D of LNG export capacity, which will require additional infrastructure to connect them to the interstate pipeline network and deliver large volumes of natural gas to liquefaction terminals. Cove Point and Sabine Pass Trains 1–4 are currently the only operational LNG export facilities in the US, but three new facilities (Freeport LNG, Cameron LNG, and Corpus Christi LNG) are under construction in the South Central region. All three facilities have associated pipeline projects that are scheduled to be completed in 2018, and EIA anticipates they will provide a combined average of 5.45 Bcf/D in export capacity.