Six months ago, if asked what the biggest challenge was facing our industry and perhaps the world, I would have said, “The transition to a low-carbon/net-zero world.”

Who knew that the biggest threat would actually be an invisible, but devastatingly brutal, enemy? And what impact will that have on our futures? Not only on our commitment to net zero but to our industry’s survival and to the industrialized world we know.

There will be many views, but as I lead a technology organization, I believe we can use this “industrial reset” to chart a new course for our industry and hopefully for our planet. This is a time for us to capitalize on the amazing collaboration we have seen locally, regionally, and globally, as society has pulled together to fight COVID-19.

Can we not put this can-do attitude into action on our biggest global challenges and work together to find a solution? While many of the changes required will be either behavioral or regulatory, a number will be technology-led—and that is where technical industries can have the biggest positive impact in the coming years.

As I look around the world, I can already see countries launching major public/private initiatives to grasp the low-carbon agenda. These are partnerships where businesses innovate and collaborate, with government backing, to create powerful collectives driving both decarbonization and economic growth.

I strongly believe this is the route we should take in the UK—forming deep collaborations to capitalize on our expertise and collective know-how to transform the North Sea into a low-carbon powerhouse.

Progress Made So Far

The good news is, we have already begun.

The UK Continental Shelf has already committed to a net-zero future in the industry’s Roadmap 2035, introduced by Oil and Gas UK.

The Oil & Gas Technology Centre (OGTC) has been supporting the industry with more than £150 million co-invested in emerging technologies in the past 3 years. And in 2019, we opened a center dedicated to the development and deployment of net-zero technologies.

We have worked closely with industry to develop a technology vision and roadmap that focuses on three big goals:

- Reducing emissions from existing operations

- Developing new technologies—including carbon capture, utilization, and storage (CCUS) and also hydrogen—to unlock the potential of our assets and expertise

- Transforming to a net-zero industry in the longer term

No one imagines this will happen overnight—the Committee on Climate Change, for example, recognizes that oil and gas production will continue to 2050 and beyond—but at the same time, it predicts massive growth in other sectors, most notably in offshore wind, blue hydrogen, and CCUS.

The current confluence of global challenges, therefore, offers a huge opportunity for the industry to set itself new goals on efficiency, performance, carbon footprint, and the transition to a net-zero future.

At the OGTC, we are already working with industry on a host of technologies that impact our operational footprint, improve efficiency, reduce the number of workers offshore or time required offshore, and improve performance.

Technologies including Total and Taurob’s autonomous offshore inspection robot, Air Control Entech’s inspection drones, Eserv’s scanning/modelling capability, nonintrusive inspection technologies by Eddyfi, Mistras, and Sonomatic, and a host of data analytics technology from IMRANDD, OPEX Group, and Global Design Innovation (GDi), which are all driving improvements in how we operate our facilities.

These technologies are ready now, and they are already making a big difference. And in this world of social distancing and reduced manning, these technologies need to be deployed rapidly to reduce our costs, reduce our operational footprint, and improve our performance.

Having an active hopper of projects which improve performance, reduce costs, and reduce operational carbon impact is good. We have been successful in our first 3 years by driving development and deployment of new technology in the North Sea. This has resulted in more than 20 technologies being commercialized, more than 100 field trials completed, and 200 technologies being invested in.

But this is not enough. We need a new approach for the future.

A New Approach

To deliver a net-zero future, we must be braver.

Offshore wind continues apace, but in other sectors, the future market is not clear.

We talk of a need for large volumes of carbon sequestration and this is repeated in many company scenarios and strategic plans. The Committee on Climate Change identifies a need for the UK to capture and store between 75–175 mt CO2 annually by 2050 if it is to meet net zero. We also hear of a “new” and significant hydrogen market as it becomes the solution to our heavy transport and industrial power demands.

Domestic transportation will be electric. And while the EV market is emerging, it has not grown at the rate required to make a global or national impact which fundamentally changes the whole transportation system.

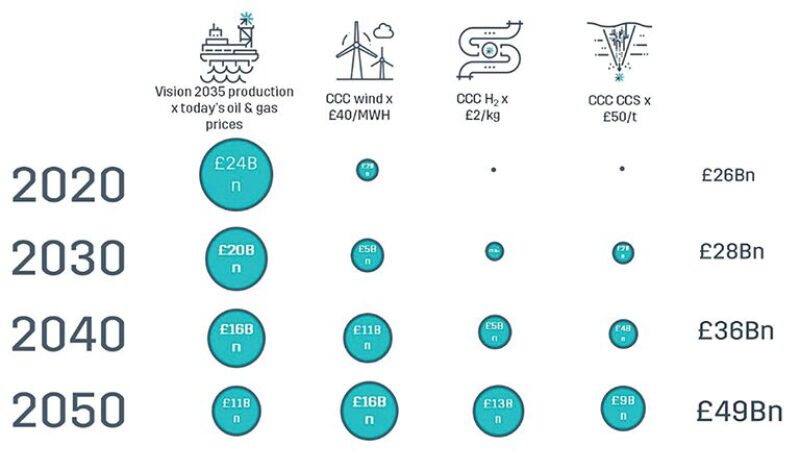

Together these three sectors—offshore wind, hydrogen, and CCUS—are predicted to dwarf oil and gas by 2050, but the overall size of the pie grows significantly from £26 billion to £49 billion. So there is room for everyone. This is not about either/or; this is about an integrated energy future for the UK.

Each presents a material opportunity to the UK, but we’ve got to grasp them—now.

So, what is required?

Well, policy is required, but so is technology. And leadership.

Offshore wind is already powering forward. We have seen incredible expansion in the sector in the past decade, but this is set to increase massively in the years ahead. The UK government has set a target of 75 GW by 2050, and this will certainly require significant deployment of deepwater floating turbines in the North Sea.

Although there are around 60 floating turbine designs, none has yet emerged as a leader, and any winning design will play into a new global market.

CCUS and hydrogen generation technologies exist too, but neither are competitive or commercial. If these markets are truly to emerge, we need competitive, flexible, replicable, adaptable technology that meets the needs of cities, regions, and industries.

And to deliver that, we need technology leadership. We need clear investment from industry, supported by both government funding and aligned government policy.

Other nations are seeing the opportunity—setting a strategy, funding collaborative, and bold projects with clear net-zero goals, building on their infrastructure or historical position. Examples include the Hydrogen Valley in the north Netherlands and the Zero Emission Energy Distribution (ZEEDS) project in Norway.

Hydrogen Valley. This 5-year, €90 million project brings together more than 30 public and private sector organizations to build and demonstrate a completely functioning hydrogen economy in one northern area of the Netherlands. Hydrogen Valley comprises four clusters, each of which will be complete by 2025, and covers the entire hydrogen chain including:

- Creation, storage, and infrastructure

- Making hydrogen a raw material for industry

- Turning hydrogen into heat and power for homes

- Using hydrogen for green vehicles

With 30 sub-projects, Hydrogen Valley is funded through a subsidy of public-private co-financing of €70 million.

Zero-emission energy distribution at sea. Annually, shipping is responsible for nearly 1 billion tonnes of CO2, or 3% of global CO2. If it were a country, shipping would be the sixth-biggest emitter after Japan.

In response to this, six Nordic companies, spearheaded by technology company Wärtsilä, have joined forces to develop a new infrastructure for green fuels for ships.

The ZEEDS initiative is a novel concept using wind and solar power to produce hydrogen, ammonia, and liquid biogas at sea, with production and bunkering initially located along the northern European shipping highway.

Other members include shipping and logistics company DFDS, shipowner and operator Grieg Star, engineering company Aker Solutions, energy firm Equinor, and EPC company Kvaerner.

Wärtsilä’s project lead Cato Esperø said such a multifaceted project requires what he calls “composite competence.” “We knew we needed energy, engineering, and construction players, coupled with power suppliers and global and Nordic shipping. What each of these different project partners have in common is a sustainable perspective.”

He points out that the partners are not necessarily competitors, but that they may be in certain contexts. The project defines most of the workflows, but partners will also work on their own initiatives. “And along the way we will of course redefine and recalibrate assignments,” Esperø said.

It’s Time To Be Bold

It is time for the UK to pursue a similar strategy. Where are our big, bold projects?

We must build on our excellent North Sea capability, skills, and extensive gas processing and transportation infrastructure to prepare ourselves for a new integrated energy future.

Through our geography and our oil and gas heritage, we have a natural lead in CCUS and wind, and it would be a tragedy if we let others seize the opportunity to build the next generation of energy technology in the UK.

Emerging from this challenging time is an opportunity to rechart our future, a time to invest in the technologies of tomorrow, and build the manufacturing capability to deliver a net-zero economy, We have an academic, research, and deployment capability that is agile and industry-led. Once we take advantage of these opportunities, then—just then—we may capitalize on the great innovative companies and capabilities we have in the UK.

The opportunities are there—the time to seize them is now.

I believe it is time for the UK to establish its major project initiatives around hydrogen and wind and create our decarbonized future. We must come out of this downturn with our sights and our investments firmly focused on a net-zero future.