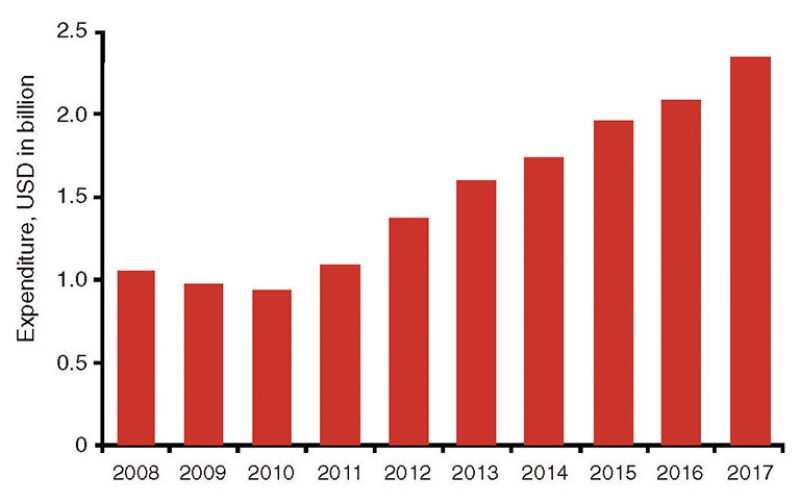

In the latest edition of its World ROV Operations Market Forecast, Douglas-Westwood expect annual expenditure on work-class remotely operated vehicles (ROV) operations to increase from USD 1.6 billion in 2013 to USD 2.4 billion in 2017, a compound annual growth rate (CAGR) of 11.3%. The market is expected to total USD 9.7 billion over the period, a growth of 79% over the previous 5 years.

Expenditure is forecast to increase more than operational days because of the move toward deeper waters and more complicated offshore field development programs, which demand higher specification, higher cost ROVs.

Drilling support of exploration and appraisal (E&A) and subsea development wells is the main ROV activity demand driver, accounting for 75% of the total expenditure between 2013 and 2017. Construction support accounts for 20%, and repair and maintenance for 4%.

The largest regional market is expected to be Africa with other important players identified as Latin America, North America, and Asia. The Golden Triangle, comprising Brazil, the Gulf of Mexico (GOM) and Africa, is forecast to account for the majority of global ROV demand, but Asia will see significant growth.

Global ROV Supply

The current industry structure is the result of mergers and acquisitions over more than 30 years. The world fleet of work-class ROVs currently consists of 1,102 units operated by 25 companies. Of these, the top 10 players dominate the market with almost a 60% share.

Oceaneering, the largest operator with 316 ROVs in its fleet, accounts for approximately 30% of the global total with its operations primarily used for drilling support. In its third quarter 2013 release, the company anticipated adding 20 units to its fleet. Longer term, the company believes it could add from 90 to 95 incremental vehicles (55 drilling support, 40 vessel support) by 2017, based on its current market share and outlook for demand.

Drivers and Indicators

While ROV support is needed in a variety of industries, such as research, military, and offshore wind power, its primary use is by the oil and gas sector. Thus, the global demand for energy, of which oil and gas makes up 57%, is the main underlying driver behind ROV demand.

Oil and gas demand has grown substantially in recent years, increasing by 31% since 2000 and primarily driven by the developing world. Demand is forecast to continue growing significantly as oil, particularly in its use within the transportation industry, cannot be easily substituted by alternative energy sources. As supply from conventional resources becomes limited, production will have to move to deeper water, creating a greater need for ROVs as activity in the subsea market increases.

Some ROVs may be installed on a vessel, where they are essential, but not used on a full-time basis. However, others may be in continuous use, particularly those used for drilling support. Therefore, there can be significant differences between the total available days of the ROV fleet and actual operational days.

ROV support activity is driven by a number of supply and demand side factors, including:

- Increasing offshore exploration, appraisal, and development, and the move to deeper water drives expenditure on ROV drilling support operations.

- Increasing installation of subsea equipment and hardware requires greater ROV construction support expenditure.

- A large and growing offshore infrastructure of platform installations, subsea wells, flowlines, and cables drives the use of ROVs in the subsea inspection reliability and maintenance (R&M) market.

Market Forecast

ROVs are used for subsea construction support and drilling support activities, as well as the R&M of existing subsea infrastructure.

Drilling Support

ROVs are needed to support the drilling of E&A and development wells. While E&A wells account for the largest proportion of ROV drilling support (69% in 2013), subsea development wells are expected to experience higher growth during the 2013 to 2017 period, increasing at a CAGR of nearly 10%.

Construction Support

Subsea construction activities that require ROVs include the installation of subsea trees, umbilicals, and flowlines, TMFJ (templates, manifolds, flowlines, and jumpers), subsea processing, floating production, storage, and offloading vessel mooring and risers, and trunkline installation.

Expenditure on construction support is expected to increase USD 166 million from 2013 to 2017. Africa will be the largest regional market with construction support spend expected to grow at a CAGR of 20%. In 2013, TMFJ accounts for the highest proportion of total ROV construction support demand at 62%, and umbilicals and flowlines at 18%.

Repair and Maintenance

The demand for ROVs to be used for R&M activities is driven by the increasing volume of installed subsea hardware. However, R&M only accounts for a small proportion of the total ROV market (4% in 2013 and 2017).

Regional Analysis

Africa

Africa will remain the largest market from 2013 to 2017, with total capital expenditure (Capex) forecast at USD 2.4 billion. Angola and Nigeria in West Africa are significant deepwater locations, forming part of the Golden Triangle of deepwater oil and gas. The discovery of new deepwater provinces offshore East Africa will further drive the demand for ROV operations in this region.

Latin America

Latin America is forecast to be the second largest market with a total spend of USD 1.9 billion during the 5-year forecast period, predominately due to the large number of discoveries and developments offshore Brazil, where deepwater reserves are increasingly being developed and the region is also moving toward developing its ultradeepwater (>2,000 m) pre-salt reserves. For these reasons, expenditure in Latin America is forecast to grow at the fastest rate of all the regional markets at a CAGR of nearly 16%.

Asia

Asia is expected to be the third largest ROV operations market during this period, with expenditure forecast to total nearly USD 1.4 billion. Production was previously restricted to shallow-water activity, but there are now a number of projects that are producing or underway in deepwater areas. Thus, demand for ROV support has increased in recent years, and since 2009, Asia’s spend on ROV activity has been higher than that in North America, its previous competitor.

North America

Issues related to the Macondo incident in the GOM in April 2010 meant that during the 2009 and 2010 period, the North American oil and gas industry faced a significant downturn, particularly when coupled with the global economic recession. However, an increase in offshore drilling rig numbers and forecast subsea hardware expenditure will drive demand for ROV support to pre-Macondo levels in 2013. The majority of ROV activity will be in the GOM, where major deepwater oil finds are expected to drive the growth of ROV demand.

Australasia

From 2009 to 2012, the demand for ROV support offshore Australia remained steady, but a sharp increase in demand in 2013 meant ROV days almost doubled from their 2012 levels. Large shallow-water gas developments now dominate subsea activity, so Australasia’s demand is set to decline substantially over the forecast period.

Eastern Europe and Former Soviet Union

The region is forecast to be one of the smallest markets in terms of ROV activity. However, it will experience some growth in demand from 2013 to 2017, as required ROV support days grow at a low CAGR of 6%. Demand within the region will be driven almost entirely by trunkline installation and E&A well drilling.

Middle East

The Middle East is the smallest ROV operations market, accounting for less than 2% of the global total ROV days in 2013. As a predominantly shallow-water region, the growth in activity levels forecast in the other regions is not expected to be mirrored in the Middle East. Expenditure on ROV support in the Middle East is forecast to fall substantially, almost halving as it decreases to USD 27 million in 2017. ROV activity in this area is almost entirely driven by trunkline installation and E&A well drilling support.

Norway

Norway is expected to see Capex associated with ROV support activity decrease from USD 119 million in 2013 to USD 113 million in 2017, mainly due to the maturity of the region with little deepwater development and its existing production concentrated in relatively shallow waters.

United Kingdom

Another mature market, the UK is dominated by shallow-water developments and is anticipated to see a small increase in ROV support demand at a CAGR of 4%. Drilling support expenditure is forecast to be the most significant part of this rise.

The Rest of Western Europe

The rest of western Europe, a mature region with limited deepwater activity, is forecast to have low levels ROV demand. Growth is expected to be steady at a CAGR of less than 4%.

Conclusions

Increasing water depths of oil and gas industry operations is the key driver of future work-class ROV demand as more activity becomes beyond the reach of divers.

Globally there is strong growth for work-class ROV operations from 2013 to 2017 with drilling activity forecast to account for the largest proportion of demand. As ultradeep waters are drilled and developed, there will be a growing need for high-powered ROVs, increasing the total spend.

The deepwater Golden Triangle regions of Africa, Latin America, and North America are expected to continue to hold the most long-term growth potential and the biggest markets. Asia will also show significant growth.

Kathryn Symes joined Douglas-Westwood in 2013 after working for an investment firm in China. She has researched the oil, gas, and renewables sectors, including FPSO research, oilfield services, and offshore and onshore logistics projects. She holds an MS in economics from Queen Mary College University of London.