A new paper from ADI Analytics examined the feasibility of using natural gas to fuel oilfield production equipment. It predicted there are unique circumstances in which it could become an attractive alternative to diesel fuel, although it will not become a standard in the immediate future.

In the paper (“Innovations that Simulate Gas Demand and Develop New Markets: Fueling the Oilfield with Natural Gas”), Uday Turaga, CEO of ADI Analytics, and Brandon Johnson, a senior analyst with the firm, wrote that US natural gas supply will continue to be abundant and cheap thanks to a dramatic increase in dry shale gas production over the past few years. ADI projects that US dry shale gas production will reach around 50 Bcf/D by 2021. Natural gas availability will incentivize use in a wide range of applications, including fueling energy-intensive oilfield equipment.

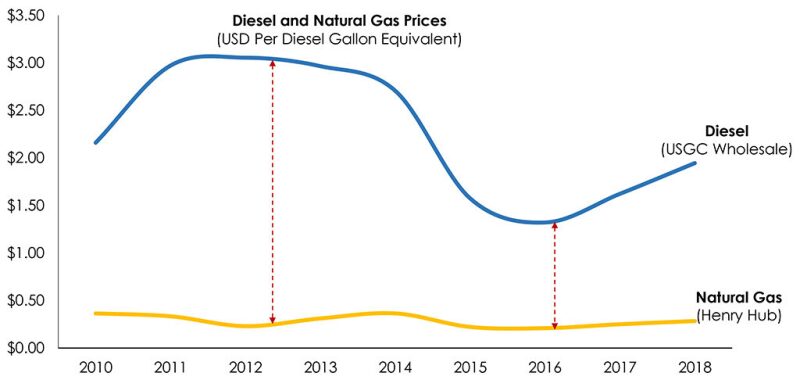

At a presentation held during the World Gas Conference in June, ADI argued that a wider price gap between natural gas and diesel fuel will drive interest in using natural gas.

The paper looked at the issues surrounding the procurement and processing of four types of natural gas—field gas, pipeline/sales gas, liquefied natural gas (LNG), and compressed natural gas (CNG)—in various shale plays. Despite an abundant supply of natural gas in the US, they wrote that not all plays have sufficient infrastructure to fully utilize each source, and that each play presents its own challenges.

Turaga and Johnson said that a lot of field gas cannot reach the market because of a lack of gas gathering facilities. Additional pipelines would have to be built in order to gain access to nearby natural gas pipelines or gas processing plants.

For instance, the Bakken is challenged by limited pipelines, gas processing, and storage capacity; counties with the most drilling activity are located on average about 50 miles away from the nearest gas processing plant. Most active counties in the Eagle Ford are located between 20 to 30 miles from the nearest gas processing plants, making it easier for field gas to hit the market.

The Marcellus and Utica plays could benefit most from natural-gas-fueled equipment, given their extensive gas processing and underground storage infrastructure. Rising natural gas production through 2025 will require new pipelines. The Haynesville Shale has significant gas processing capacity, some underground storage capacity, and “attractive” breakeven costs.

The Permian Basin has high gas processing and underground storage capacity across its key sub-plays, but it is limited in LNG and CNG capacity. However, the addition of several new pipelines driven by Mexico and LNG exports from the US Gulf Coast has boosted the area’s existing pipeline capacity, and like the Eagle Ford, many gas processing plants are located near the most active drilling areas in the region.

Turaga said that associated gas in the Permian is significant because of the level of drilling activity in the region, but the increase in pipeline capacity may be a sign that natural gas usage is not a high priority for operators there.

“It is possible that you could see some development and growth of natural gas usage in the oil field there, but there’s so much concentration of resources happening in the Permian that it’s possible that the need to develop the infrastructure there is not as acute as in some of the other plays,” he said.

Turaga and Johnson estimated that building new LNG capacity at gas processing plants would cost between $600 and $1,000 per ton in capital spending. They wrote that new CNG stations will be cheaper, in part because the US has a lot more CNG capacity and that capacity is more evenly distributed across the country, but it would still require significant capital spending.