We could have borrowed from Gabriel Garcia Marquez’s Love in the Time of Cholera to title this piece, “Oil & Gas in the Time of Coronavirus.” But that would only recognize the coronavirus disease of 2019 (COVID-19) and its impact on oil demand and ignore the black swan in the concurrent supply shock posed by Russia’s refusal to hyphenate itself with OPEC again in cutting oil production.

Broader uncertainties from an election year in the US and growing investor clamor for shale profitability and energy transition initiatives add further, even if now less-urgent, uncertainties. We at ADI instead see the "perfect storm” as a better metaphor for the collective impact from the Russian-Saudi spat and COVID-19. Metaphors and clever writing aside, how should we think about this perfect storm? We try to address this here with our firm’s research and consulting work.

Why are We Here?

The oil markets—led by Saudi and OPEC through the majors and the shale operators to the traders and analysts—were blindsided by Russia’s refusal to cut oil production with OPEC in a year when oil demand growth was expected to decline independent of the coronavirus.

Russia made some noise about OPEC cheating on its commitments but abandoned its 3-year alliance with OPEC primarily to harm US shale supply, which has been, as such, constrained by rising investor disenchantment. Larger geopolitical reasons such as US sanctions on Rosneft and Nord Stream 2 also motivated Russia, which is today in a stronger economic position relative to the 2014 oil price crash.

Surveying the Damage

Unwilling to lose market share and also force Russia to return to negotiations, Saudi announced plans to raise production from 9.7 million B/D to 12.3 million B/D starting April 2020. It also doubled down on its bet by offering discounts of $4/bbl to $8/bbl on its production. In solidarity, the United Arab Emirates will increase supply by 0.8 million B/D.

Russia plans to increase production too but only by 0.5 million B/D as it is limited by sanctions on its oil trading. In addition, incremental supply growth may come from Libya once the outage there ends along with some small production growth in other places. At this rate, collectively, the market in 2020 will be oversupplied by 3–5 million B/D and global inventory will surpass 400 million bbl over the next few months (see Exhibit 1 for one scenario variant).

However, two reasons make estimating this supply-demand balance difficult.

1. Oil demand destruction from COVID-19 is highly uncertain and today ranges from 0.6 to 1.2 million B/D for all of 2020. First-quarter oil demand alone likely fell more than 3.5 million B/D led by lockdowns in China that are spreading rapidly to US and Europe. Peak demand slump estimates range even more wildly from 3.5 million B/D to as much as 10 million B/D, likely peaking in the second quarter of 2020.

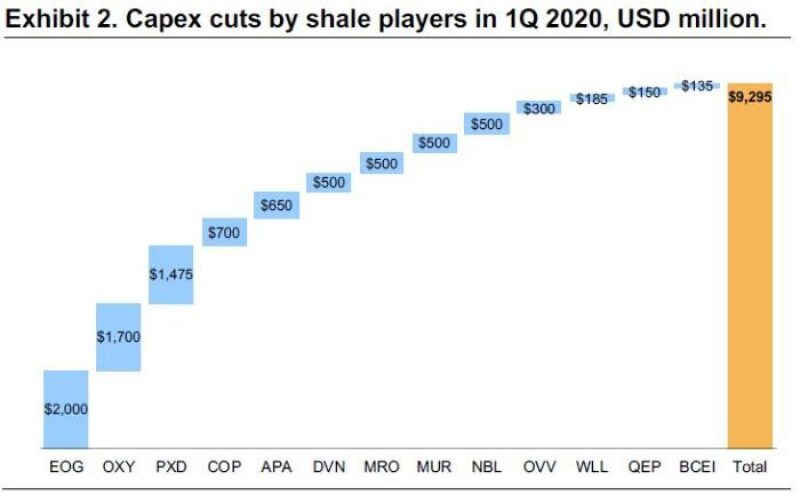

2. Operators will cut production as oil prices plumb new depths—Brent was below $25/bbl on 18 March and WTI barely at $20—but the extent is uncertain. But we do know that most of those supply cuts will likely happen in the US. Acknowledging their role as swing producers, publicly listed shale operators have started cutting capital spending with most reductions averaging 25 to 35% (Exhibit 2).

Worryingly enough, corresponding production cuts are small for those who have disclosed those details, suggesting that operators may be trimming drilling but will continue completing their well inventories, limiting the supply impact. The last oil price crash was followed by supply cuts that exceeded 1 million B/D over 15 months beginning in late 2014. The shale industry will need to deliver much deeper cuts this time—think around 2 million B/D through 2020 as opposed to growth forecasts of 0.6 to 0.9 million B/D—in order to keep oil prices from falling and staying at marginal cash costs.

What Happens Now?

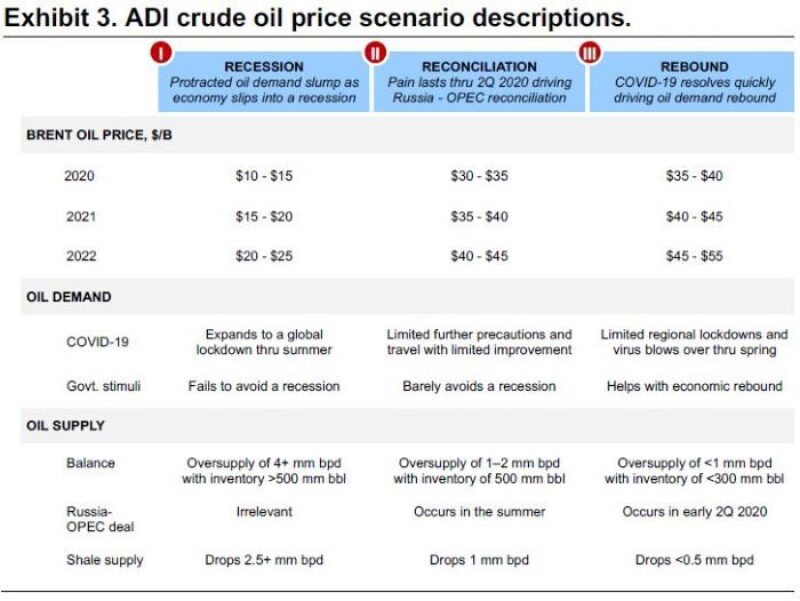

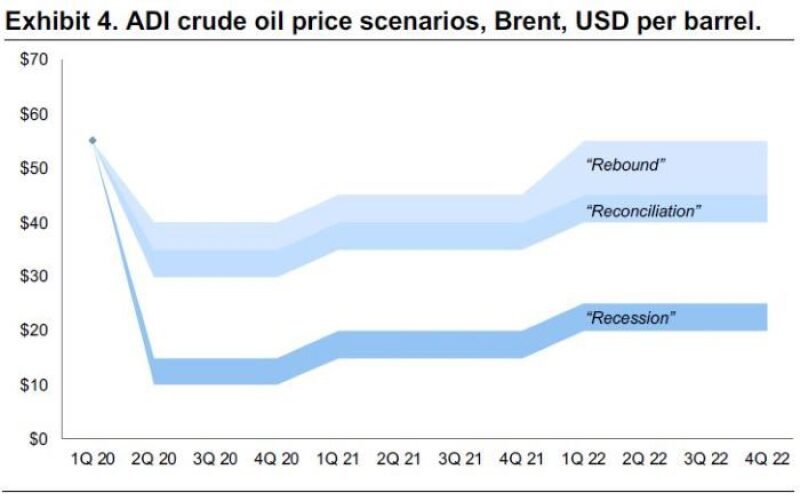

ADI has developed three scenarios (Exhibits 3 and 4) of what may happen going forward.

1. “Recession” is our most pessimistic outlook where oil demand suffers a protracted slump as the global economy slips into a recession as COVID-19 lockdowns spread and persist through the summer of 2020. Oil prices will test new lows and stay close to the marginal cash cost of $10 to $15/bbl through most of 2020. They will rise slowly to $25/bbl in 2022, just barely above the marginal cash costs. There will most likely be government stimuli as well as a deal between Russia and OPEC, but they will be irrelevant as the damage will be too severe.

2. “Reconciliation” is where we forecast a moderate level of pessimism around the global economy, COVID-19, and oil prices, which hover in the low $30s/bbl in 2020 and rise up to low- to mid-$40s by 2022. In this world, we stay at the current or slightly expanded levels of regional lockdowns, Russia and OPEC don’t do a deal until June, and government stimuli help avoid a recession but the world slips into an economic slowdown.

3. “Rebound” is our most optimistic scenario, given the current situation, where oil prices attain high $30s/bbl in 2020 and rise up to $45 to $55/bbl in 2022. A lot of things need to come together for this scenario to pass. The current set of lockdowns do not spread and they and COVID-19 blow over through the spring, Russia and OPEC come to a deal in the next month or two, and government stimuli prove to be highly effective and support an economic rebound. Even so, the aftershocks from COVID-19 and the Russia-OPEC spat linger through larger oil inventories and lead to low oil prices in the near- to mid-term.

So What?

None of these scenarios will come to pass as forecast. But a number of implications recur across our three scenarios, and the oil and gas industry may consider paying attention to them.

1. Oil and gas companies should prepare for an average oil price of $20 to $30/bbl for 2020. Modest improvements will come in 2021 with recovery only in 2022.

2. There is limited upside for oil prices through most of 2020 unless Russia and OPEC agree to a deal within the next several weeks. As Saudi Arabia ramps up production, the global oil inventory will surge and any price rise will have to wait until those inventories are depleted. Further, nearly two-thirds of US shale production has been hedged at ~$55/bbl for 2020 and is unlikely to fall at current prices.

3. Russia and Saudi Arabia both have sufficient financial resources to weather a protracted period of low oil prices. This limits the probability of a deal in the near term.

4. US shale production will fall – only by how much is up for debate. Even if hedges protect US shale operators through 2020, sharp cuts will come in 2021. Unlike the oil price crash of 2014–2016, there is limited private equity appetite to buy distressed operators. As a result, operators that are small or hold undifferentiated acreage will face significant distress.

5. North American natural gas producers will be an unlikely beneficiary of this oil price crash. As light tight-oil supply falls so will associated gas production, which has driven over 50% of gas supply growth in North America in recent years. This reduction in the growth of gas supply should help Henry Hub pricing.

6. However, some of this will be limited by caps on natural gas demand growth that will come from delays to the second wave of LNG export projects in the US.

7. Refiners’ have gone from starry dreams of a “golden year” thanks to IMO 2020 to a nightmare scenario of cutting refinery runs as refined product demand grinds to a crushing halt due to COVID- 19 lockdowns around the world. Downstream companies with complex refineries, strong linkages to export markets, mature commercial trading teams, and integrated petrochemical assets will weather through these times but other refiners will struggle.

8. Midstream companies will face challenges with product exports, in particular, light tight oil, which will have to be discounted extensively to find overseas buyers. Support for existing and new capital projects will, of course, decline. Finally, we anticipate investor flight to quality based on contract portfolios.

9. Traders and majors with strong commercial organizations will likely benefit across at least two scenarios—reconciliation and.rebound—with limited prospects in the recession scenario.

10. Shipping and logistics players with tankers, terminals, product storage tanks, and blending capabilities may benefit in this environment as a contango market drives interest and demand for storage. Our research and consulting teams at ADI recognize that these are difficult times for the oil and gas industry and its various segments as they grapple with a broad range of market, economic, and policy uncertainties. As a result, we are developing in-depth scenarios for each of the various oil and gas industry segments including upstream (onshore shale, onshore conventional, and offshore), midstream (NGLs and gas processing), LNG (small- and large-scale), refining, and petrochemicals and plastics.

These scenarios model various aspects of COVID-19, the oil price crash, and government stimuli and forecast in granular detail price, margin, and competitive implications, risks and challenges, and opportunities. Contact us at info@adi-analytics.com to learn more about ADI’s “Oil & Gas in the Perfect Storm” scenarios.

Uday Turaga is the CEO of ADI Analytics. He may be contacted at t_uday@hotmail.com.