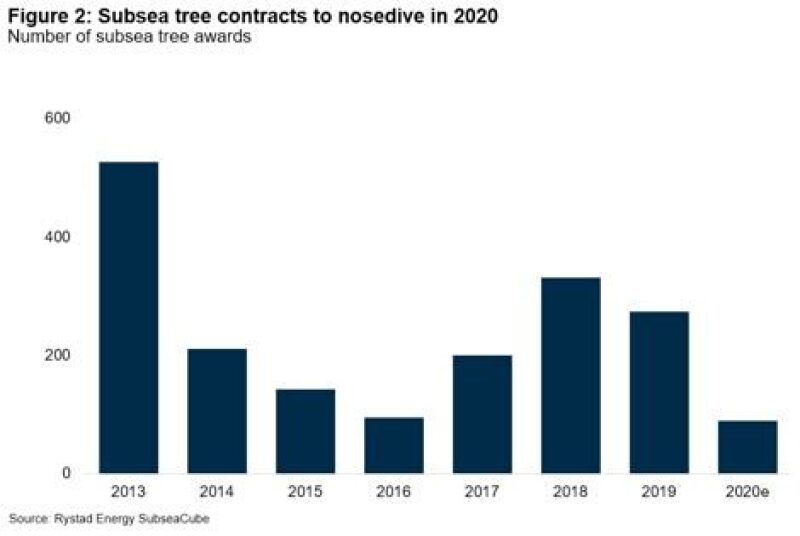

While a year with less than 200 subsea tree awards seems uncommon in the subsea market, a year with less than 100 subsea tree awards is an even rarer sight. It has only happened once before since the turn of the century, in 2016 following the oil price crash of 2014–2016. Rystad Energy now forecasts that we might be on our way to revisit these extremely low numbers again just after 3 years of recovery.

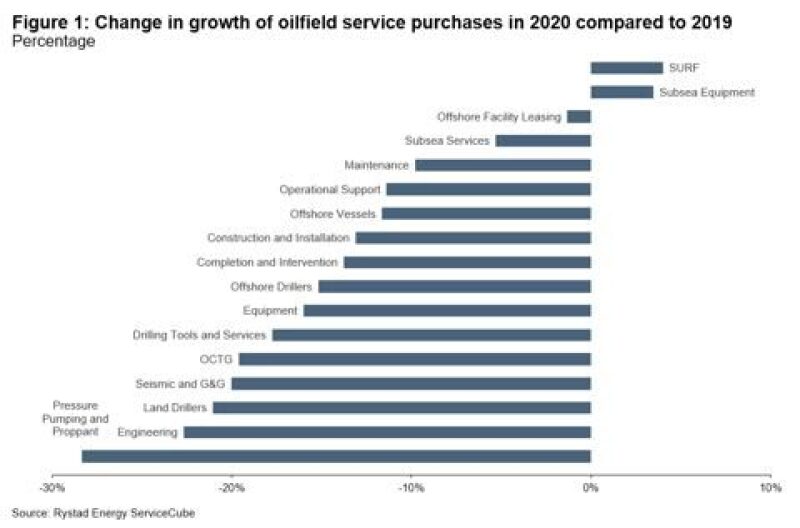

With COVID-19 casting a shadow over the world’s oil consumption, the average oil demand for 2020 is expected to clock in at 89 million B/D, an 11% drop from the demand levels seen in 2019. This has in turn led the oil price to drop significantly since the beginning of the year. On top of this the oil and gas industry also faces challenges related to operations, logistics, quarantine, travel, etc. due to the threat of a COVID-19 outbreak among workers as well as the lockdown measures imposed by several governments. In our April Supply Chain newsletter we covered a range of topics including how we see service prices develop in 2020 and whether we expect only one FPSO project to move ahead this year to how we see rig utilization plummeting over the next few years. With most segments expected to face a double-digit decrease in expenditure, the year 2020 looks bleak for all segments in the oilfield service industry.

The subsea market is by no means shielded from the crisis. For 2020, the sector might have a revenue cushion from already-sanctioned projects currently under development, but as we discussed in our April newsletter, we expect investments sanctioned this year to be even lower than the bottom of the last downcycle in 2016. Major offshore projects are being pushed out by operators, and for those that are still on the table, service companies might struggle to secure financing in the current market. Considering the challenging environment, Woodside’s contract award for the Sangomar project off the coast of Senegal might be the only major subsea tree award in 2020.

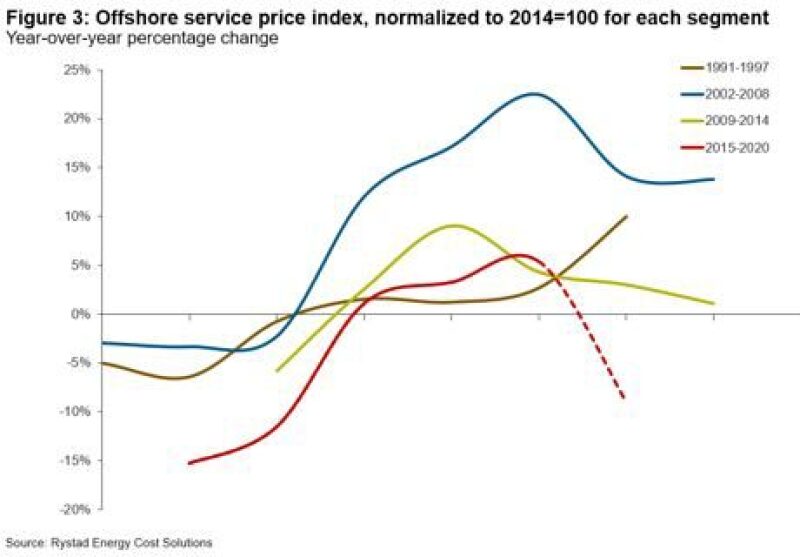

2013 was a fantastic year for subsea tree awards. However, the good fortunes of the subsea players did not last long as the tree awards plummeted down in line with the oil-price crash in 2014, falling below the 100 mark in 2016—which is the lowest number of subsea trees awarded during this century. From 2016, the market started recovering, with 2018 and 2019 both seeing close to 300 subsea tree awards. However, with the latest market downturn starting March 2020, we again expect extremely low numbers for this year, after only 3 years of recovery. Looking at the service price index for the offshore supply chain, this 3-year cycle is set to go down in the history books as the shortest cycle yet.

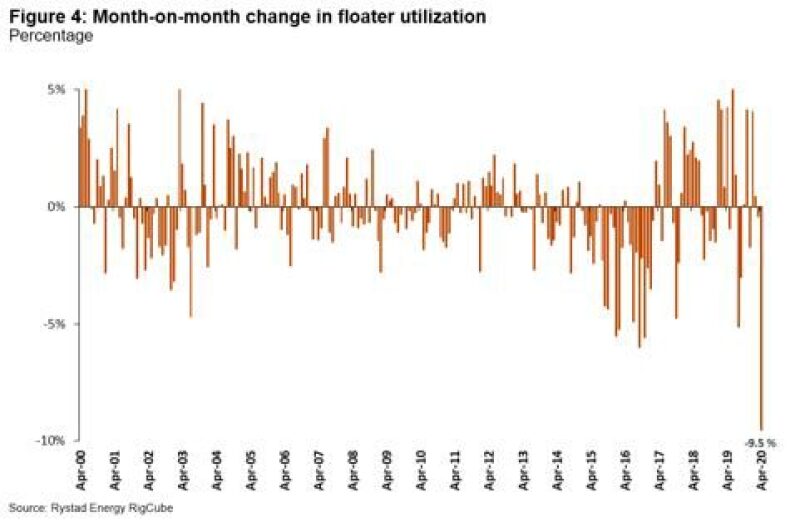

We have discussed how rig utilization is set to plummet over the next years in our April newsletter, with the uncertainty brought upon by the COVID-19 outbreak taking its toll. We are seeing alarming numbers from April as the market faces postponed drilling programs, suspended rigs and cancelled contracts. After a flat development in rig utilization from January to March, global utilization for offshore rigs dropped over 7% from March to April. In terms of prices, looking at historic data from 2000 onwards, this 7% drop is the largest monthly percentage change in utilization that the rig market has seen in this time period. Low floater utilization is an indicator of low deepwater activity, and the April drop in utilization is even larger for floaters than the general market, being close to 10%.

The year 2020 is set to be a gloomy year for the subsea players in terms of contract awards, but there might be some light at the end of the tunnel. As lockdown measures start to ease globally and oil demand picks up pace, we expect to see oil prices increase gradually. Many big projects that were previously planned to be sanctioned in 2020 will likely come back to the table in the coming years and with that bring with them a substantial subsea scope, aiding a recovery of the subsea market.