It was meant to be another boom year. After a record 70 million mtpa of new LNG capacity was sanctioned in 2019, at least as much capacity was lined up for final approval this year and next. Instead of a feast of new projects, there’s a famine.

Developers, cash-strapped by the collapse in oil and gas prices, have pushed back on capital-intensive pre-final investment decision (FID) LNG projects. Massimo Di Odoardo, WoodMac’s global head of gas analysis, identifies three other factors.

The outlook for LNG demand. We are bullish, anticipating LNG demand doubles over the next 20 years, driven by Asia’s economic growth and increasing penetration—particularly where policy supports gas over coal. Our view isn’t dissimilar to Shell’s that the LNG market grows at four times the rate of oil demand in that period.

Our base case forecasts global LNG demand grows by over 50% from 370 mtpa in 2020 to 550 mtpa by 2030. Allowing for projects already under development, there’s a supply gap of 102 mtpa to be met by pre-FID projects which need to be on stream by the end of this decade.

But there are risks to our demand view. Gas demand has held up relatively well through the COVID-19 downturn, certainly compared with oil. The pace and shape of economic recovery though is far from clear and so, too, LNG demand growth in the next few years. Longer term, intensifying interest from policy makers and investors in new technologies, including green hydrogen and carbon capture and underground storage, casts doubt on the sustainability of demand growth.

The rising influence of spot LNG prices on project economics. The traditional oil-price-linked contracts and firm offtake agreements that have supported the financing of new projects are fading into history. Many projects today rely on equity lifting, with joint venture partners taking the LNG into their own portfolios. The attraction is flexible volumes that can be sold to any buyer and capture the best price.

But it also means rising exposure to spot LNG prices. Japan spot LNG prices have ranged from over $11/MMBtu in 2018 to as low as $2.10/MMBtu early this year, underlining the volatility and risk in running an open spot gas position.

Scrutiny of carbon intensity. Environmental, social, and corporate governance (ESG) has leapt to the top of the agenda for LNG producers and buyers alike. LNG’s track record on emissions isn’t good. Inert gases including CO2 must be removed before liquefaction and typically are vented into the atmosphere. Liquefaction itself is energy intense, usually fueled by produced gas.

In the future, carbon footprint will be one factor determining how attractive an LNG project is to developers and buyers, and will influence the price it can command. New projects will have to be squeaky clean: developers will seek to electrify the liquefaction process (renewables where possible) and capture waste gases. Project economics will also be affected by carbon price assumptions.

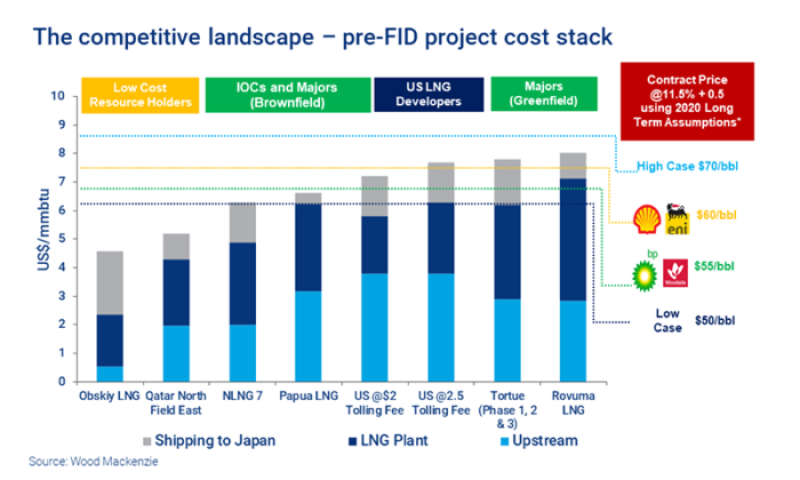

Which pre-FID projects will fill the 102-mtpa supply gap in 2030? First up are the mega-trains of Qatar’s low-unit-cost North Field East, which should be sanctioned in the coming months. This project on its own will absorb 32 mtpa, negating the need for new supply from other sources until the late 2020s and pushing out FIDs for projects elsewhere by 2 to 3 years. Qatar believes it has another 16 mtpa up its sleeve at North Field South that it could also develop.

So contestable demand for the rest is 70 mtpa at best in 2030. A dozen or more projects from PNG, Australia, Mozambique, West Africa, Russia, and North America, with combined capacity of more than 150 mtpa, will be vying for their share.

The costs of integrated projects are discounted at 12%. Segmented projects—at 10% discount rate for LNG plant, 15% discount rate for upstream. Taxes are included. US upstream assumption = 115% X Henry Hub ($3.29/MMBtu—equivalent to average of long term H1 2020 Henry Hub forecast between 2026 and 2035) Note: The reference prices indicated in the above chart with company logos indicate the long-term prices used by companies for the purposes of valuing their assets. Assumed to be in real terms (2020) from 2023.

How can prospective developers gain a better understanding to help support their big decisions? Wood Mackenzie’s new Global Gas Model Next Generation allows investors to analyze global gas market fundamentals and price formation; how LNG cash cost economics, coal-to-gas switching and shipping costs shape price differentials between the US, Europe, and Asia markets; and how the cost stack for pre-FID projects evolves over time to meet any particular demand scenario. The model provides a framework to understand a project’s profitability under current market uncertainties.

Simon Flowers is chairman and chief analyst for Wood Mackenzie and author of The Edge.