Oil and gas supply chain companies have seen their profits squeezed since the E&P cost cuts of the previous downturn – and just as the industry could finally hope for better days, the Covid-19 pandemic caused the value of 2020’s awarded contracts to slump to a 16-year low of $446 billion. At the same time, the transition to cleaner energy technologies is accelerating and many suppliers will have to make existential changes to survive. Rystad Energy has evaluated who is better prepared.

The 2020 drop in awarded contracts was a steep slide of 30% from 2019’s $641 billion. The last time the industry saw a lower total was in 2004, when awarded contracts totaled $317 billion. The supply segment that declined the most in 2020 was construction and installation with a 59% drop, followed by equipment (-46%), stimulation (-45%), and engineering (-41%).

Drilling tools and services, seismic and geological and geophysical (G&G), oil country tubular goods (OCTG), land and offshore drillers, subsea umbilicals, risers, and flowlines (SURF), and subsea equipment all declined by between 30% and 40% last year. The supply segments that fared better (relatively speaking) were operational support with awarded contract value dropping 9%, subsea services (-9%), and offshore facility leasing companies (-11%). The only supply segment that managed to score better than in 2019 was maintenance, rising 2.1% in 2020 to $72 billion.

The past year has been a stormy one for the oilfield services industry. Out of the handful of contracts awarded, Brazil and Norway offered the lion’s share. Meanwhile, several already awarded contracts came under scrutiny, with many contractors receiving requests for revised prices.

Even if 2021 proves to be a better year, the service industry will struggle to replicate former glories, especially as the entire energy industry is being pushed to embrace the energy transition and offer less-carbon-heavy solutions.

Suppliers now face the existential question: Can they build viable, long-term strategies on their current operating model and market exposure? This question is becoming more urgent as stakeholders such as the financial industry discriminate against oil-and-gas-related securities due to inherent energy transition risk—the idea that value is at risk as markets deteriorate during the energy transition.

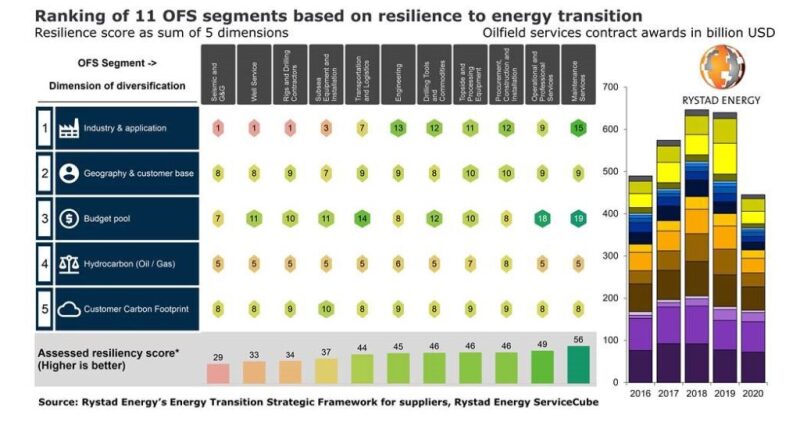

Rystad Energy’s consulting team has developed a strategic framework to help clients navigate this jungle of communication and decision-making. Among the different elements of the service, we have developed an assessment test that gauges the inherent resilience to the energy transition for supply chain companies on an as-is basis.

The test is tailor-made to produce individual scores for each company and can also be applied on a sectorial basis. In this article, we are sharing a scorecard for some higher-level sectorial results, using five key dimensions that all represent an inherent source of resilience to the forces of the energy transition. The ultimate resilience score is the sum of the 0–20 interval scores from the five individual dimensions.

The maintenance segment ends up as our most resilient sector by far, thanks to its already diversified nature and its high reliance on OPEX budgets, enjoying a resilience score of 56 (100 is max). Operational and professional services also scored high (49), helped by resilient budgets. Transportation and logistics, drilling tools and commodities, topside and processing equipment, and the engineering, procurement, construction, and installation (EPCI) sector were close, scoring between 44 and 46.

In the other end of the scale, seismic and G&G struggles with a setup highly geared toward oil and gas and largely relies on a very exposed customer budget item, namely exploration, ending with a score of just 29. Other struggling sectors were well service (33), rigs and drilling contractors (34), and subsea equipment and installation (37).

In three of the five dimensions the scores of each sector seem relatively even. This is due to the large number of industry participants in each sector, which gives a broad distribution of exposure across geographies, customers, hydrocarbon types, and customer emission intensities. However, our experience is that individual companies can find themselves being outliers along these dimensions.