Since 2006, the fastest growing sector in the oil and gas industry has been the midstream sector. This is primarily due to the energy renaissance over the last decade, which was driven by a dramatic increase in the production of crude oil, natural gas, and natural gas liquids from the upstream sector. The midstream sector assets connect supply to demand, and the resulting growth in production sparked a massive need for billions of dollars in new capital expenditures to fund the building of this critical infrastructure in transportation, storage, and natural gas processing. Master limited partnerships (MLPs) have provided one important means of financing this explosive growth.

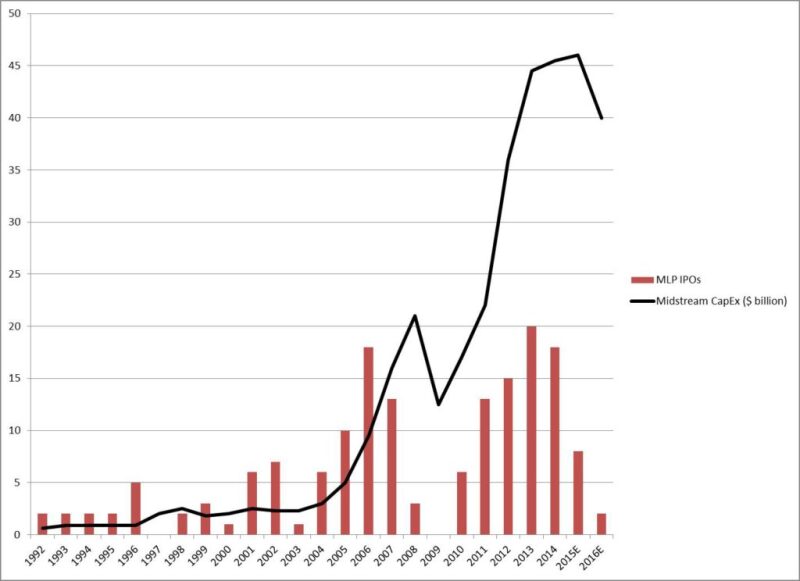

Fig. 1 illustrates the midstream capital expenditures (Capex) in billions of dollars and the number of MLP initial public offers (IPOs) per year from 1992 through mid-2016. Note the dramatic increase in both Capex and IPOs that began around 2005 with the shale boom. Between 2008 and 2015, the Capex had doubled from roughly USD 20 billion to USD 45 billion. More than 50% of the Capex in each of these years was spent on oil and natural gas transportation. While the downturn that began in 2014 has slowed the rate of growth, major investments are still needed in midstream to fund Capex over the next 2 decades. ICF International forecasts a range from USD 471 billion (low scenario) to USD 621 billion (high scenario) of new capital expenditures will be needed over the next 20 years, which translates to USD 22.5–30 billion per year on average (See North American Midstream Infrastructure Through 2035: Leaning into the Headwinds, ICF International, 12 April 2016.) http://www.ingaa.org/File.aspx?id=27961&v=db4fb0ca

MLPs

An MLP is a publicly traded partnership that is structured as either a state law partnership or limited liability corporation. Shares in the MLP are called “units” and the shareholders are called “unitholders.” The units are traded on public exchanges such as the NYSE or NASDAQ. MLPs are taxed as a partnership and therefore, they pay no corporate level tax.

The first MLP was launched by Apache Oil Company in 1981. The popularity of MLPs grew quickly due to the tax advantages, liquidity of the investment, and attractive yields to investors. The US Congress restricted the types of businesses that could form MLPs in 1987. To qualify as an MLP, at least 90% of the gross income had to come from natural resource activities as defined by Section §7704 of the Internal Revenue Code. Many oil and gas MLPs left the market in the late 1980s through the 1990s due to the energy downturn. By 2000, there were around 20 MLPs and the number of MLPs operating in midstream began to steadily increase at this point due to new growth in the midstream sector. In 2008, the qualifying income was changed to include ethanol, biodiesel, and other alternative fuels. By November 2016, there were roughly 117 MLPs operating in the oil and gas industry.

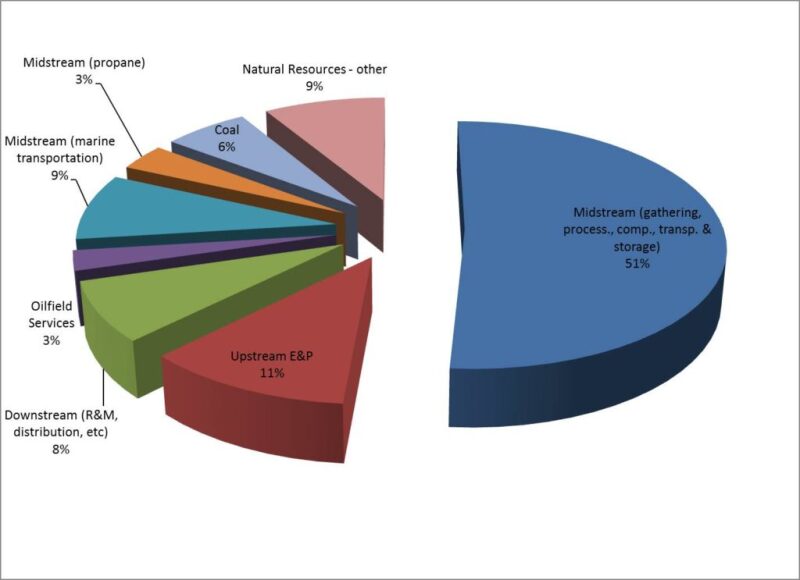

Fig. 2 illustrates the current types of MLPs that operate in the oil and gas industry. As shown, 51% operate in the midstream activities involving natural gas gathering and processing, or transportation and storage of crude oil and natural gas. Another 12% operate in the midstream activities of marine transportation, and transportation and marketing of propane. Only 11% of MLPs operate in upstream—exploration and production.

The MLP structure offers many advantages to the company (known as the sponsor) that forms the MLP (although not all MLPs have a sponsor). By forming an MLP, a sponsor can “monetize” a group of assets by selling these assets to the MLP structure at a higher valuation than is currently reflected in the parent’s valuation. At the same time, the sponsor retains control of these assets by owning the general partner, who operates the MLP and has 100% of the voting rights. This helps raise capital for the company to expand growth. Consequently, MLPs have been key to financing growth in the midstream sector over the past decade. The key advantage of the MLP structure is the avoidance of double taxation on distributions since the MLP is a pass-through entity. What this means is the income passes through and is taxed only at one level —that of the general partner or individual partner (i.e., the unitholder). Distributions from C-corporations, on the other hand, are taxed twice, once at the corporate level and then again at the investor level when the stock pays a dividend. Other advantages of MLPs are the deferral of taxation for the sponsor on asset drop-downs, incentive distribution rights that accrue to the general partner, and a reduced cost of capital.

There are many advantages to investors in MLPs. First, MLP units offer an attractive yield, which is very desirable when other investment opportunities offer lower yields. Second, there is no corporate level income tax as mentioned above; therefore, distributions are only taxed once. Third, distributions are paid quarterly, and for most MLPs, are fairly stable over time since many midstream activities are fee-based (lower risk) and have lower exposure to commodity prices relative to upstream. Fourth, a large part of the distributions is shielded from taxes because some of the distribution is considered a return of capital. The unitholder will not be taxed on these amounts until the units are sold.

Conclusion

MLPs have been instrumental in providing the capital needed to build new infrastructure in the oil and gas industry over the past 2 decades. MLPs are unique to the US and offer many financial benefits not only to the companies that form an MLP, but also to investors as an attractive investment vehicle. MLP management teams have demonstrated financial flexibility and creativity in the recent challenging times. In particular, most midstream MLPs have been resilient and exemplified the sustainability of the MLP business model.

For Further Reading

Energy Finance and Economics: Analysis and Valuation, Risk Management, and the Future of Energy, Editors: Betty Simkins and Russell Simkins, John Wiley & Sons, Inc., 2013.